U.S. solar builders face delivery woes in pull away from China

Customs delays, tariff uncertainty and soaring global demand have hiked solar costs and delayed projects as the U.S. weans itself off Chinese dependence.

Related Articles

A fall in U.S. solar installations in 2022 and rising project prices show how a ban on products made from forced labour in China along with other U.S. trade policies are pushing the U.S. further away from President Biden's goal of a decarbonised power sector by 2035. Utility-scale solar installations fell by 23% as delays pushed projects into 2023 while average solar PPA prices in Q4 rose 33% on a year ago.

The Biden administration's Uyghur Forced Labor Protection Act (UFLPA) prevents the import of goods produced using forced labour in China’s Xinjiang Province, including much of the polysilicon used in solar panels.

The vast majority of U.S. panel imports come from the four Southeast Asian countries of Cambodia, Malaysia, Thailand and Vietnam, but most contain materials and components produced in China. The Xinjiang region produced almost half of all global polysilicon output in 2021, according to U.S. Department of Labor estimates.

UFLPA checks have blocked panel imports at the U.S. border, delaying projects and driving up project costs. U.S. Customs and Border Protection (CBP) had detained 1,000 panel shipments by early November 2022 and pricing platform LevelTen Energy estimates this figure is now closer to 1,400.

Importers must prove the entire value chain is free from production in Xinjiang and a lack of precise guidance from the CBP means that panels are taking months to clear customs, industry experts say. Importers must pay the cost of warehousing panels which amounts to around $250,000 to store 10 MW of panels for 90 days, LevelTen said.

The UFLPA and other U.S. trade policies present the greatest short-term risks to U.S. solar deliveries, Tom Starrs, Senior Director – Government and Public Affairs at developer EDP Renewables, told Reuters Events.

EDPR strongly supports the intent of the UFLPA but “the lack of guidance and lengthy delays at the border in reviewing and releasing shipments is causing unanticipated costs and project delays," he said.

Probing suppliers

The delivery challenges come as activity is set to soar on the back of tax credits set out in President Biden's 2022 Inflation Reduction Act. Solar installations must triple to 60 GW/year by the middle of the decade to meet the President's goals, the Department of Energy (DOE) said in a report in 2021.

Solar manufacturing capacity by country, region

(Click image to enlarge)

Source: International Energy Agency's Report on Solar PV Global Supply Chains, August 2022

The UFLPA requires visibility into labour practices along the solar value chain. Workforce transparency is more difficult for polysilicon and particularly challenging for pure silica and its predecessor quartzite, due to less availability of workforce information further up the supply chain, Gia Clark, Senior Director, Developer Services at LevelTen Energy, told Reuters Events.

In addition, polysilicon ingots often use a mix of material from various producers, so precise origin documentation is not always available, Clark said.

Most developers are adapting their procurement strategies to reduce dependence on Chinese materials and many are hiring third-party auditors to validate the origin of their imports.

Finding new suppliers and implementing tracing protocols is expensive and time consuming for developers who are already combating inflation, high interest rates and lingering supply chain disruption following the pandemic, Clark noted.

Developers have also delayed projects due to impending U.S. import tariffs which whipped up market uncertainty and pricing risk during a probe by the U.S. commerce department. From June 2024, a number of Chinese suppliers in Cambodia, Malaysia, Thailand and Vietnam will be subject to tariffs after the commerce department found they were circumventing tariffs on China.

Soaring global demand for solar is adding to the challenges faced by U.S. developers. Equipment such as inverters, trackers and transformers can be sourced from U.S. or European suppliers, but lead times have increased as Europe also hikes renewable energy targets.

The time it takes to develop a 100 MW solar project in the U.S. from greenfield to starting construction has increased from 18-24 months to 36-48 months, Kevin Smith, CEO, Americas at developer Lightsource bp told Reuters Events.

Procurement decisions must be made two to three years prior to the start of construction, rather than six to 12 months as previously, Smith said.

Together, the supply chain challenges have increased project capital costs by 20-30%, he said.

U.S. factories

While US tariffs are helping to shift polysilicon production and ingot and wafer manufacturing away from China, the Biden administration’s inflation act is accelerating domestic capacity.

The act includes tax credits for clean energy factories as well as solar and wind projects. In one example, South Korea's Hanwha Q Cells plans to invest $2.5 billion to build a solar power manufacturing value chain in the U.S. state of Georgia that will increase its U.S. production capacity from 1.7 GW to 8.4 GW by 2024, the company said last month.

The buildout of new U.S. polysilicon, ingot and wafer facilities will be more challenging than expanding module capacity and it will take years for U.S. solar suppliers to meet domestic requirements. Meanwhile, the European Union is also ramping up support mechanisms in a bid to retain investments and expand its supply base.

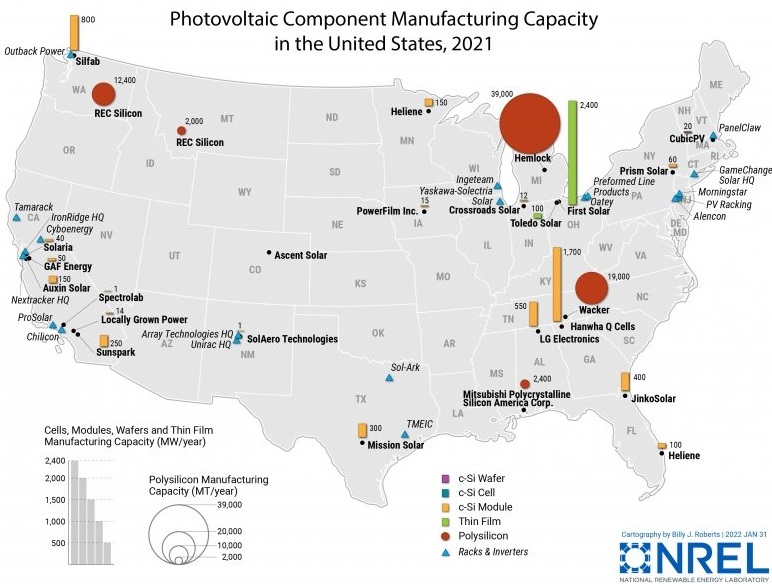

U.S. solar manufacturing facilities in 2021

(Click image to enlarge)

Lightsource bp sources most of its solar panels in the U.S. from domestic group First Solar but is having to look to other countries to fulfil its demand. Lightsource bp has contracted for more than 20 million solar panels through 2028 and is considering imports from Southeast Asia, Turkey and India, Smith said.

The tax credits in the inflation act could make U.S. manufacturing costs competitive with imports, but manufacturers are also likely to command a price premium because they can help developers meet domestic content requirements for tax incentives and reduce their exposure to trade restrictions, Starrs noted.

Ultimately, the switch away from China “will result in higher costs but lower risks, and ultimately stronger and more predictable supply chains," he said.

Reporting by Neil Ford

Editing by Robin Sayles