US utility’s deferred reactor clean-up shows cost pressure on early closures

Omaha Public Power District (OPPD) has opted to defer decommissioning of the 479 MW Fort Calhoun Station (FCS) to delay high upfront spending and protect consumer prices but industry experts warn of cost-escalation risks.

Related Articles

The 43-year-old Fort Calhoun PWR plant in Nebraska has a license to operate until 2033 but the plant is among a number of U.S. reactors which are to be closed earlier than planned amid tough power market conditions and a lack of state support. The plant, owned by OPPD and operated by Exelon Generation, is to be shut down October 24.

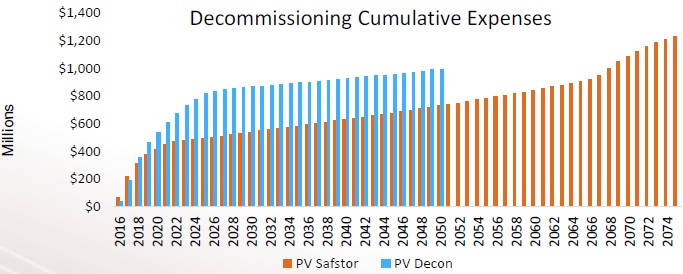

The majority of current U.S. decommissioning projects are being carried out under the “SAFSTOR” method of deferred decontamination rather than the DECON option of immediate action. SAFSTOR requires operators to complete the entire decommissioning process within 60 years, providing more flexibility on the allocation of resources, but it also incurs regulatory and cost escalation risks.

Many operators have chosen the SAFSTOR method as the closures are taking place long before plant licenses expire and they have not accumulated enough funds to cover the high upfront costs involved with decommissioning projects, Thomas S LaGuardia of leading cost estimation firm LaGuardia & Associates, told Nuclear Energy Insider.

Project management costs can represent as much as 55% of total decommissioning costs, with 20-25% allocated for dismantling and around 25-30% for waste disposal, he said.

OPPD has so far built up a decommissioning trust fund of $388 million for FCS, but this represents only a third of the estimated decommissioning cost of $1.2 billion.

By using SAFSTOR, OPPD can defer D&D while it builds up the DTF through annual company contributions, federal spent fuel payments and returns on fund investments, curbing electricity price rises for consumers, Chris Averett, OPPD spokesman, told Nuclear Energy Insider.

Source: OPPD

OPPD supplied 18.2 TWh to around 360,000 customers in 2015 and the utility aims to avoid electricity rate increases for the next five years and keep rates 20% below the regional average, Averett said.

OPPD currently owns 3 GW of installed generation capacity including coal, nuclear and renewable energy assets.

Around 700 personnel are employed at FCS and deferred D&D offers flexibility in the timing of performing decommissioning work and means staff can be reallocated to other roles or projects, Averett said.

Cost risks

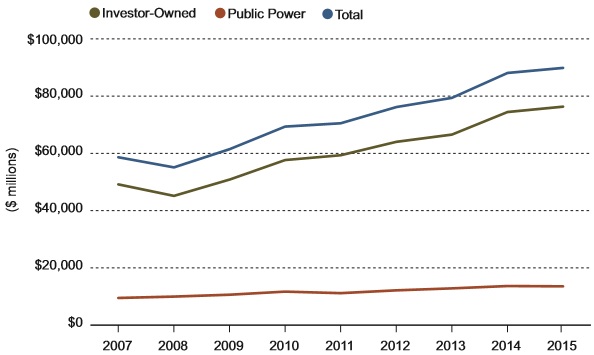

U.S. decommissioning cost estimates have risen year-on-year as operators have faced fresh site-specific challenges and evolving regulation.

Decommissioning cost estimates in current dollars

Source: Callan Institute's '2016 Nuclear Decommissioning Funding Study.'

While most operators have chosen to defer D&D activities by using SAFSTOR, operators can benefit from using the alternative DECON approach as it allows then to shift the financial liability for decommissioning activities to a contract company, La Guardia said.

Although SAFSTOR requires a minimal initial outlay and delays spending on the main expenses, licensees need to manage NRC regulations and the site’s nuclear liability over several decades.

Geoffrey Rothwell, Principal Economist at the OECD’s Nuclear Energy Agency, said operators should start decommissioning activities as early as possible as the deferral of D&D exposes operators to delay-related costs, investment risks and loss of crucial expertise as workers leave the industry.

A major advantage of carrying out D&D activities immediately is that current operations staff have in-depth knowledge of plant specifics which avoids unnecessary work-arounds, Rothwell told Nuclear Energy Insider in an interview last month.

By deferring D&D activities, operators raise the chance of chemical or radiation leaks spreading and the introduction of stiffer regulation, he said.

While decommissioning cost estimates have risen, rates of return for DTFs have been lower than expectations, and operators which have accelerated closure plans should leverage current staff expertise and optimize decommissioning schedules to allocate decommission fund portfolios so the “liquidity matches your plans,” Rothwell said.

In one recent example, Southern California Edison opted in 2014 to use DECON on its 1.1 GW San Onofre units 2 and 3 to dismantle, manage the used fuel and restore the site within 20 years at an estimated cost of $4.4 billion. However, the operator had accumulated a significant DTF of some $4.1 billion.

Optimizing SAFSTOR

FCS accounted for more than 34% of OPPD’s annual electricity generation prior to 2012 and a study by consultancy Pace Global showed that replacing FCS with alternative sources would save the utility between $735 and $994 million over the next 20 years.

The analysis also confirmed that new renewable capacity within OPPD’s portfolio would help the operator comply with the U.S. Clean Power Plan (CCP), which is due to come into force on 1 January 2022 and does not include credits for existing nuclear plants.

OPPD currently generates a surplus to its customers’ requirements and only 44% of electricity from FCS would need to be replaced through new sources such as wind or solar power, gas-fired power or wholesale market purchases, according to the company.

Rebalancing the portfolio in favour of renewables would reduce exposure to fuel price volatility and long–term options for replacement capacity will be detailed in an Integrated Resource Plan which OPPD aims to complete by the end of the year.

OPPD’s decommissioning schedule will start with the transfer of nuclear fuel to the spent fuel pool by mid-November. The fuel will be left to cool for around 18 months and then be packed in dry casks and transferred to an Independent Spent Fuel Storage Installation (ISFSI), a process that takes a further five to six years.

The operator license can only be terminated once D&D of the FCS is completed and the Department of Energy has collected the spent fuel from the site.

By Karen Thomas