US hydrogen strategy takes shape

The United States’ plans for building a clean hydrogen industry are taking shape after the release of an ambitious roadmap, though analysts caution that its success depends on how it is implemented.

Related Articles

The U.S. government has passed a slew of measures aimed at creating a low-emissions hydrogen economy, including the Infrastructure Investment and Jobs Act in 2021, which includes $8 billion for hydrogen projects, and the Inflation Reduction Act (IRA) in 2022, which provides generous tax incentives.

In July, the Department of Energy released a request for information (RFI) to invest some $1 billion to stimulate the demand side of the hydrogen equation in recognition that, for the industry to succeed, there must be offtakers as well as producers.

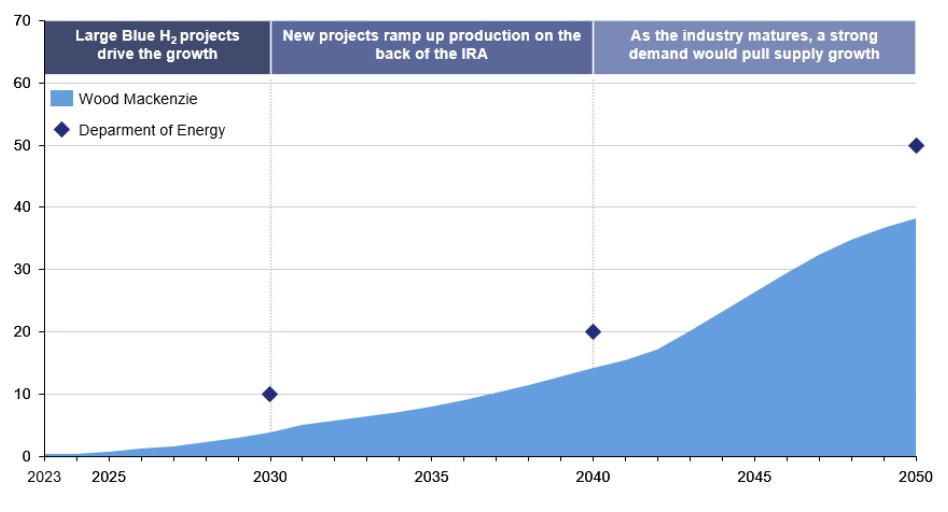

Strategic opportunities exist to produce by 2030 annually 10 million tons (MT) of clean hydrogen – where carbon intensity is below 4 kg of CO2/kg of hydrogen well-to-gate – 20 MT by 2040, and 50 MT by 2050, according to the ‘U.S. Nation Clean Hydrogen Strategy and Roadmap’.

“The report is meant to be a living strategy that provides a snapshot of hydrogen production, transport, storage, and use in the United States today, as well as an assessment of the opportunity for hydrogen to contribute to national decarbonization goals across sectors over the next 30 years,” the roadmap says in the introduction.

It aims to do this through three key strategies; target strategic, high-impact uses for clean hydrogen; reduce the cost of clean hydrogen and; focus on regional networks.

The strategy also emphasizes that activities would include collaboration across multiple federal agencies, as well as industry, academia, and environmental groups.

Positive reception

The strategy has been largely well received by analysts.

“I think it's very comprehensive and it recognizes the opportunities that are out there, but also the current and future challenges, both for the government and the industry,” says Hector Arreola, Principal Analyst at Wood Mackenzie.

However, while Arreola applauds the general direction of the plan, he believes the pace at which it is expected to unfold is too optimistic under current conditions.

“In the short term, meaning up to 2030 which has a 10 MT per annum target, we just don't see that the industry is going to get there,” he says.

“In order for a particular volume to be online by 2030, projects pretty much have to have been announced already. The math is very simple and to get to the target, we need to see the projects, which we’re not seeing.”

Wood Mackenzie forecasts that adoption will gain momentum after 2040 and clean hydrogen production reaching 38 MT a year by 2050.

This is primarily due to renewable power cost, electrolyzer load factor, and a slow decline in capital expenditures for electrolytic hydrogen, projected to be around $1,600/KW by 2030, the consultancy says.

U.S. Low-Carbon Hydrogen Supply

(Click to enlarge)

Source: Wood Mackenzie

Uncertainties over additionality, temporal matching, and geo-location in carbon intensity calculations could substantially impact the level of production subsidies and, consequently, the adoption rate, Arreola says.

On the demand side, the strategy notes hydrogen should be initially adopted where it can yield greatest economic benefits and decarbonization potential, such as industries already using hydrogen produced from fossil fuels, including clean ammonia, methanol, steel production, and sustainable aviation fuel.

“A lot of investments are being confirmed for refining, for ammonia, for methanol … industries that wish to convert their existing high-density carbon hydrogen demand and substitute it with low-carbon hydrogen. It makes economic sense there,” Arreola says.

Continued uncertainty

The lack of confirmed, large hydrogen projects – beyond the many Power Points and PDF strategies that have flooded from companies over the last couple of years – is a reflection of continued uncertainty over how and under what circumstances the subsidies will be allocated.

However, professional services company Deloitte, which has been helping to advise companies navigating the prospect of developing an economy behind low-carbon-intensity hydrogen, says companies are working hard to make sure they are ready for both regional domestic consumption and – in some countries – eventually exports.

“For now, the challenge that everyone is facing is creating a bankable proposition to get to Final Investment Decision (FID) on the projects that they've either announced or started working on. And we're still a ways from that,” says Geoff Tuff, hydrogen practice leader at Deloitte US.

Companies want to demonstrate that they can get to FID, even on small scale projects, and to start production, he says, adding that while there is no massive clean hydrogen industry yet, the opportunity is certainly there.

“There's a broad-based recognition that the subsidy money is nice, but there are complexities in how they're going to administer the grants; it just may not be worth it to slow things down and complicate things while everyone else is getting into production mode.”

The billion dollars available to stimulate the demand side is a drop in the ocean compared to what will eventually be needed, but the economics on existing projects are tight enough that every cent on the kilogram can make a difference, he says.

Constructing a hydrogen sector from virtually nothing will require leaders to work on managing risks in different ways, striking contracts in different ways, and thinking about asset lifecycles in different ways.

“One of the things that we’ve come to conclude given all our global work in the space is that clean hydrogen is not a technology problem anymore. It's a business model problem,” Tuff says.

By Paul Day