US wind O&M thrust creates new roles, supplier networks

U.S. wind operators will invest in repowering, digital tools and remote technologies in the coming decade, supported by deeper service and spares networks, analysts and suppliers told New Energy Update.

Related Articles

The phasing out of the U.S. federal production tax credit (PTC) is set to profoundly impact wind industry spending and employment trends. The 10-year PTC is set at $23/MWh for projects completed by 2020, then falls by 20% per year. U.S. installations are forecast to peak at around 13 GW in 2020 and fall to around 6 GW in 2021-2028, according to data from the U.S. Department of Energy (DOE), gathered from multiple forecasters.

U.S. wind capital spending is set to surge from $12 billion in 2018 to an average $14 billion per year in 2019-2021 as developers race to meet PTC deadlines, research group IHS Markit said in its recent '2019 Wind Power Plant Benchmarking in North America' report.

This installation surge will drive growth in operations and maintenance (O&M) spending during the 2020s as capital spending slows, IHS Markit said.

U.S. annual wind O&M spending is set to rise by 50% by 2030, to $7.5 billion, it said.

“There is going to be shifting in priorities from building as much as possible to optimizing these projects," Max Cohen, associate director in IHS Markit's renewable power division, told New Energy Update.

IHS Markit predicts a transition in employment opportunities from construction to O&M jobs in the “early 2020s.” Wind O&M employment in North America will rise from 6,000 in 2019 to 9,000 by 2030 and total wind jobs will climb, it said.

The U.S. Department of Labor is similarly bullish, predicting a 57% growth in wind service technician jobs by 2028, making it the fastest growing profession.

Surging states

O&M market competition has soared as operators seek new ways to lower costs. Falling turbine margins have prompted suppliers to expand in the O&M market. Many larger fleet operators have built up in-house O&M teams to gain greater control over operational risks and maximize economies of scale.

Key concerns for workers are the geographic spread and the required skills base of new job openings.

O&M spending and employment growth is expected to be highest in the Great Plains and upper Midwestern states, such as Iowa, Oklahoma, Kansas, Illinois, Colorado and Minnesota, where installations have soared, IHS Markit said.

"By 2030, these six states will increase annual O&M spending by $1.3 billion," it said.

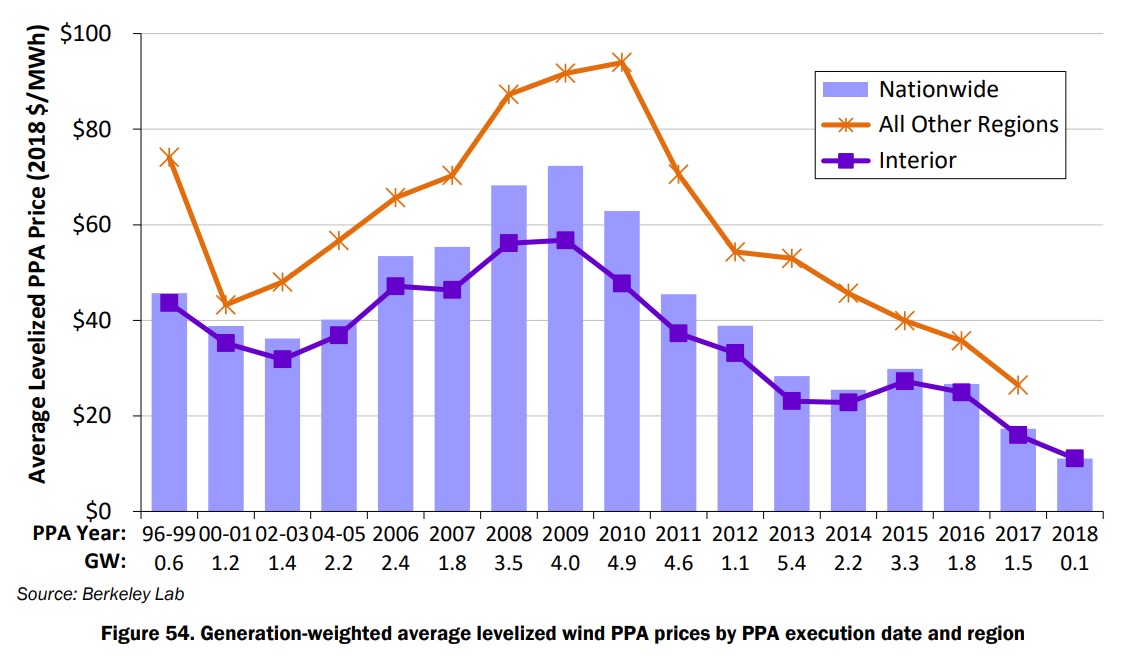

Rapid buildout in the U.S. Interior has already sliced installation and O&M costs. Average wind PPA prices in the U.S. Interior fell below $20/MWh in 2017 and many are now pricing well below this level.

US average wind PPA prices by region

(Click image to enlarge)

Source: DOE's 2018 Wind Technologies Market Report.

Developers in the U.S. Interior have benefited from more favorable wind resources, large areas of flat land which can accommodate large-scale projects, and transportation access to growing regional manufacturing hubs, the U.S. Energy Information Administration (EIA) said in a 2018 research note.

This regional buildout has also hiked O&M efficiency as operators have leveraged local spare parts, equipment and labor resources. Unplanned failures can cost up to $30,000 per turbine per year and spare parts and logistics costs represent around 50% of direct costs, Wood Mackenzie said in a recent report.

In 2018, O&M costs in the MISO, SPP, and ERCOT U.S. Interior markets were 35% lower than costs in California's CAISO market and 15% lower than costs in New York's NYISO, according to an earlier study by IHS Markit.

Going forward, high-growth O&M markets will attract more "specialized" service providers that can assist with less common repairs or a particular turbine technology, or provide a new innovative solution that helps to reduce downtimes, Michael McNulty, Associate – Power, Gas, Coal and Renewables, IHS Markit, said.

These services allow asset managers to sign a lower cost O&M contract and call on niche maintenance suppliers when issues occur.

As build rates decline in the 2020s, manufacturers may reorient supply chain resources towards the spare parts market, McNulty said.

This could result in more local warehouses and supply networks for faster spare parts distribution, he said.

Bigger blades

Many operators have chosen to repower operational turbines with newer, higher performance models to boost output and extend PTC support.

GE Renewable Energy, Vestas and Siemens Gamesa have repowered almost 5 GW of U.S. capacity since 2017 and plan more than 4 GW more by the end of next year.

The shrinking PTC window is spurring many operators to repower assets half-way through their provisional 20-year lifespans.

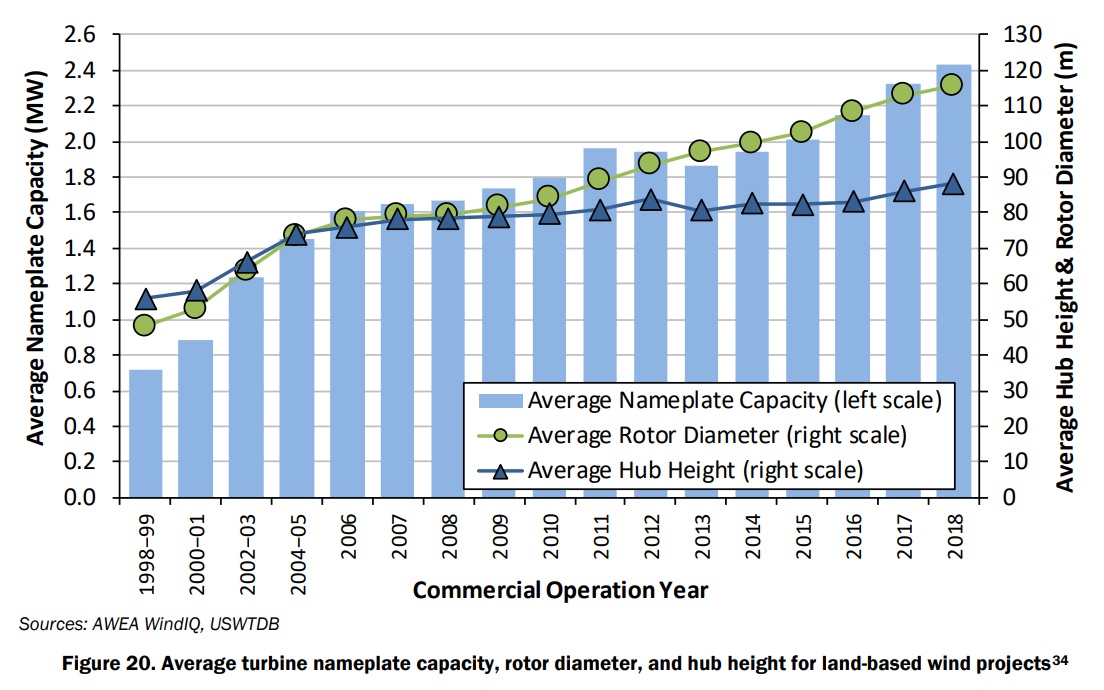

Average US wind turbine nameplate capacity, dimensions

(Click image to enlarge)

Source: DOE's 2018 Wind Technologies Market Report, National Renewable Energy Laboratory (NREL).

In some cases, repowering projects can increase annual energy production (AEP) by a quarter, leading turbine suppliers told New Energy Update in August. Suppliers predict further improvements in turbine technology could offset falling PTC income and extend repowering demand into the 2020s.

Larger capacity turbines will be a key economic driver, David Jakubiak, spokesperson for Acciona, Nordex' largest shareholder, said. Acciona recently launched a takeover bid for the group.

“As the new generation of 5X MW onshore wind turbines are made available by manufacturers like Nordex, developers will have opportunities to either repower existing projects or develop in areas with a high demand for power but lower wind resource,” Jakubiak said.

Further innovations will boost turbine performance in the coming years. Technology improvements will include self-diagnosing turbines, real-time output maximization and crane-less maintenance, Denver Bane, Onshore Wind Services Strategy Leader at GE Renewable Energy, told a conference in April.

Digital edge

Larger fleet operators are deploying data analytics to improve O&M efficiency and minimize labor costs.

Data analytics and sensor technology allows wind operators to implement preventative maintenance strategies and reduce unplanned outages. Advanced analytics and machine learning can help operators optimize logistics costs, spares management, and energy production.

Operators are also deploying drones to inspect large wind and solar sites. Combined with advanced imaging technology, drones can pinpoint faults and dramatically cut inspection times.

Drone inspections will become more valuable as turbine capacities grow. GE's latest 5.3 MW onshore wind turbine boasts 77 m blades and hub heights of up to 161 m. Manual inspection and diagnostics of such behemoths can take hundreds of man hours and operators can cut costs dramatically by using one operator and a high-definition drone.

Remote drone inspections also facilitate more centralized fleet operations, reducing the costs associated with local inspection teams.

"The adoption of new technology to assist in wind operations has been dramatic," McNulty said.

"Employment in wind O&M will still go up overall, but the kinds of skills required could change over time," he said.

Widespread roll-out of digitalisation and data analytics could open up new operations roles in more centralized control rooms.

"There could be more need for data analysts," McNulty said.

"These could be located anywhere, probably a corporate headquarters or perhaps a remote operations center."

By Paul Day