By

By

With Contribution from: AXA, AVIVA and Gjensidige

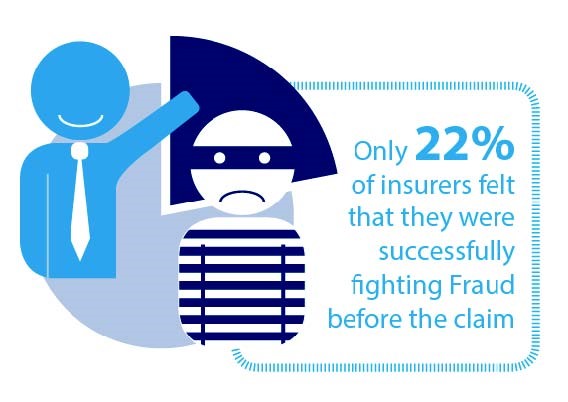

According to a survey by Insurance Nexus of over 100 insurance professionals for the Insurance Fraud Survey 2015, 33% agreed that sales teams should be more engaged in fraud detection and that application fraud was flying under the radar. Despite 67% of insurers listing fraud before the claim as one of the key priorities in their organisation, only 22% felt that they were successfully dealing with it.

Stopping fraud at the front line is proving a challenge for insurers. With a growing number of industry bodies such as the Insurance Fraud Bureau (IFB) holding data on proven fraudsters, there is a facility to reconcile data that automatically excludes habitual offenders, but this is still only a small portion of the threat posed to the industry.

Improved data gathering, a growing sophistication in marketing and operations technologies that allow companies to track the customer journey and pick out suspect behaviour are all contributing to greater fraud resistance. And yet, few feel they are successful in dealing with fraud before it reaches the claims stage. According to the Association of British Insurers, it is estimated that around £1.9bn (€2.2bn) of fraud goes undetected each year. That adds approx¬imately £50 per year to all other policy-holders premiums. Despite these huge losses, there remains a number of barriers to achieve effective front line defence against fraud.

This paper will examine what these major hurdles are and asks the opinions of three fraud experts from around the world on what steps insurers might take to stop the influx.

Detecting Priorities

The industry executives interviewed for this paper universally agreed that despite the need to make detecting fraud on the front line a priority, they were not blessed with limitless resources and had to pick their battles carefully to extract the best returns.

The Insurance Fraud Survey 2015 identified that staged accidents and application fraud were most likely to go undetected in insurance organisations and that they also presented the highest degree of threat (31% and 12% respectively). Data theft was also an issue but considered easier to trace than the other two with 18% stating it went undetected compared to 51% for staged accidents and 33% for application fraud.

This is worrisome for those seeking to halt fraud at the front line as application processing has become one area where new technologies being used to provide a better customer service are also determining competitive advantage.

On the one hand, insurers know that customers want the easiest experience possible. They want companies to know their data and autofill forms; they want rapid quotes at the touch of a button and one-click payment - ‘seamless’ is the word most often bandied about. "In the spirit of competition between carriers, it’s at the point where insurers can’t compete if they can’t do it quickly," states Gordon Rasbach, Global Fraud Management Leader at Aviva General Insurance.

There are some ‘quick wins’ to be gained with access to some basic data points. "Validating peoples’ identity and the risk we’re being asked to cover - that’s relatively simple," insists Richard Davies, Global Fraud Control Officer AXA SA, & Head of Fraud, AXA UK. "Various motor vehicle checks for example will cover that person’s accident history."

However, large insurers have systems in place and are able to access and store data to respond to customers either via the web or through a contact centre very rapidly. If the front line happens to be through the broker network, it is a different scenario.

"That is one step removed," Davies warns. "We’re relying on brokers to do what we would ideally want to. In the last three to four years the larger brokers have been pretty innovative in managing fraud risk and doing a good job of it.

But where some are struggling is in terms of resource. As a result we are letting them access our resources, for example by giving them the ability to use the same screening tools as we do, which we have delivered through the internet portal. The challenge is keeping them up to date."

Access to good clean data is going to be critical, as are the technologies to manage it. However, as always insurers must weigh up the commercial returns gained from delivering a competitive customer experience at speed and the financial risk from letting potential fraud through the net in the name of expediency.

Understanding what types of fraud pose the biggest threats to the insurer is crucial to their ability to combat it. The sheer size of the task contrasted with the resources available to combat it decree that insurers are having to pick and choose which avenues to pursue.

"It’s unrealistic to think you’re going to catch all fraud. You want to make sure what you’re getting, though, is the worst of the bunch," Rasbach advises.

"I agree that capturing the worst fraud is our target. I don’t think we have a goal of trying to catch it all. But we certainly have more opportunities to do it than we use today," adds Vera Sønsthagen, Head of the Special Investigation Unit at Gjensidige Insurance in Norway.

This can be seen from the survey where under or over coverage is experiencing quite high levels of poor detection with 21% of executives stating that they can’t pursue it, yet none of those same executives felt it actually posed a significant risk to the organisation.

Prioritising where to anticipate and pursue the fraudster is also proving a sticky issue for insurers who are keen to see the best returns. To date, this has been through pursuing them at a claims level. Diverting resources to tackle the issue at the first contact stage is a bigger education piece for executives.

"Detecting fraud during the onboarding process is not our biggest target. It’s hard to get the organisation on board with this. We are focusing instead on claims and while I think we are working at the right speed with that, it’s not plug and play - systems have to be developed to see if the rules are right. We can’t work faster than the whole organisation," Sønsthagen reveals.

Data

A data-driven industry as a whole, there was a low level of insurers reporting in the Insurance Fraud Survey 2015 that data was making responding to fraud difficult. Only 11% had problems with internal data quality while 6% had issues with data protection and privacy.

Indeed, the executives interviewed for this report largely agreed that they could access the information they needed when it came to identifying fraudsters. The creation of the Insurance Fraud Bureau (IFB) in the UK and resources such as the Insurance Fraud Bureau of Canada allowed insurers to check the status of appli¬cants using automated services and receive definitive results in real time. This could, according to the insurer’s specific risk rules, allow an immediate decision to be made whether the application was coming through the web or call centre. Exemptions in strict data protection policies also allow insurers to extract and share information on dubious characters.

It would appear that the UK and Canada at least feel that their ability to share data and identify fraudsters is at a satisfying level.

"It’s very easy to do this in the UK," Davies adds. "We have a specific exemption in the data protection act for the purposes of detecting crime. Data matching tests with the banks and others tells us we could soon be seeing indicators of fraud from a couple of months to a year in advance of when we can currently detect them, so this tells us we have to establish very strong data-sharing partnerships as an urgent priority."

However this is not the case for all insurers, Sønsthagen notes:

"It is very difficult for us in Norway because we have strict regulations when it comes to data sharing between companies. We have to use trends instead. Only when we have concrete evidence of fraud, then we can share data. If anything, it’s getting stricter - there is no IFB equivalent," she explains.

For the most part however, it seems insurers are on the right track as far as data is concerned. "We are on the right path but there’s a long way to go in terms of getting the data we need. The big hurdle that insurers have not established as well as other industries such as banks is that they don’t have enough experience yet in categorisation. What constitutes a fraud and what are consistently deemed as serious, major and minor behavioural traits. The more insurers end up sharing and considering each other’s data the sooner we will all speak the same language,” Rasbach says.

Using data to identify fraud on the front line will not right all wrongs however. Identifying regular, belligerent fraudsters is one thing, creating behavioural traits and models that allow for the discovery of hitherto undiscovered criminals is another.

"Gathering data on known fraudsters is still the best defence against fraud on the front line. There is good work going on about predicting events such as policy and claim fraud but they are far, far from maturity. It’s still very risky to rely on those on the front line," Rasbach says. "These ideas are riding a hype wave that seems higher than it actually is. The risk of false positives is far too high. At Aviva we’re being very cautious about how much the front line is exposed to analytics and tools that try to predict fraud based on propensities. In the future a big part will be finding a balance for this type of modelling."

Criminalising and deterrents

Application fraud covers a wide range of activities, from the determined fraudster at the outset to the bargain hunter keen to shave a few pounds off their premium. After all, in many cases insurance is seen as a necessary evil (particularly the case in motor and buildings with secured loans where it is mandatory) and therefore the overriding sense is to pay as little as feasibly possible for it. Comparison sites such as the UK’s gocompare.com or comparethemarket.com make it quick to see how a premium might be lessened if certain criteria are changed.

These sites certainly do not promote fraudulent activity but they greatly reduce the leg work where a customer would have previously had to go from broker to broker to achieve the same result. So begins the slippery slope where a lightly massaged set of application details that goes undetected can lead to an inflated or fabricated claim at a later date.

Detecting a burgeoning fraudster of previous clean character is very difficult purely through data, as has already been mentioned. The modelling of behaviours is not sophisticated enough to create a viable set of red flags to be investigated. However there are ways insurers can help themselves as well as helping the customer to stay on the straight and narrow.

"Aggregators are a useful data step. One thing that has been proven is that when a customer is going to commit policy fraud, the likelihood of committing claims fraud is also high. Say you’re able to see someone put a quote through in the span of two hours during which they change rating information. If there’s no intelligence that suggests they have been fraudulent anywhere else then it’s possible to use cognitive deterrents - ‘We notice you gave different answers...’ and you may want to remind them what the consequence of relying on insurance based on bogus details might be. This gives them the option of going in again and applying properly," Rasbach says.

Equally, as insurance evolves through technology and in particular the influence of telematics, the chances for opportunistic fraud and accidental criminalisation of otherwise genuine customers is limited. Take, for example, the customer who applies for occasional use of their car but the same vehicle on the same policy becomes used for long, fast, regular motorway commutes to work. Their risk profile has changed, their statements of intent no are longer true: "If that vehicle were to be involved in an accident and the insurer were to take the view that the wrong person was driving, they are quasi-criminalising what might be a genuine mistake. It’s about using your data streams in the right way," Davies states. "We need to move to a state where we offer the right service at the right time, rather than requiring our customers to spend time contacting us every time their circumstances alter."

Telematics introduces the possibility for a pay as you go type of insurance model where customers only pay for what they use, reducing the low level resentment of paying for insurance and encouraging behaviours that lower general risk as well as the risk of fraud during the insurance term.

This model is bleeding into other insurance areas such as household with the growth of by-peril. The tacit agreement that the customer will be insured for fewer risks makes it less likely for them to treat insurance as a resource when a new hall carpet is desired.

Davies also believes that by creating bespoke insurance products that are very specifically fit for a single policyholder’s purpose, it is possible to generate loyalty, which in turn lowers the risk of fraud:

"Why shouldn’t my insurer change my insurance for me depending on where I am and what I am doing? I’d like to think that they would offer me the best deal according to the risk I present them. The first insurer that changes the way they sell their products to a ‘push’ model will steal a march and their customers are likely to be loyall. This is a complete contrast to the dysfunctional way the market currently operates, where new customers are often offered better prices than the loyal ones."

By designing products that enhance customer expectation and experience there is hope that this will reduce the levels of opportunistic and application fraud that the aforementioned 33% of respondents to our survey stated was a big threat to the business.

Sønsthagen states that at the moment, her feeling is that insurance is built on trust and that insurers have to trust their customers to a certain degree at the front line: "The thought that some customers are not to be trusted is not the mainstream so it’s hard to get the focus in the organisation."

Taken at face value this might seem naive however looking at the effectiveness of positive anti-fraud content at the application stage, it may be that expensive, complex data modelling tools might not be required. As proposed in ‘Nudge theory’ (where consumer behaviour can be modified through a series of seemingly small steps, there are relatively easy decisions that can be taken to encourage people to remain on the straight and narrow.

Conclusion

Where data exists to pinpoint existing fraudsters, insurers are becoming more able to discover and eliminate their threat at the front line. Advances in technology mean that whether first contact is via web and automated services or in touch with the staff of a contact centre, fraud can be detected in real time at the point of application.

The struggle comes in identifying and dealing with fraud that has no trail. Be it experienced fraudsters who have avoided detection or the more insidious oppor¬tunistic fraud embarking on the slippery slope of application fraud as they massage policy details to find attractive premiums - these continue to leave insurers scratch¬ing their heads.

There is an acknowledgement that modelling and predictive technologies are growing up to meet this challenge but their efficacy is far from proven yet. This may be behind the reason that many organisations prefer still to focus on claims-based fraud investigations.

Until predictive analytics in front line fraud detection becomes a reality, there are still tactics insurers can deploy to protect the organisation. Tailoring products to encourage customer loyalty rather than pandering to the lowest price trend is one avenue to consider. Content at the point of application reminding customers the implications of – if not falsified – then inadequate cover is another.

One interviewee stated that trust was important in the insurance sector. Perhaps the levels of fraud currently experienced are in part down to a recent inabil¬ity by the insurers to foster it among their customer base. Improving product and customer relationships beyond the point of quote may go some way to re-establishing that trust, delivering a sense of value rather than obligation for the customer. This leaves an opportunity for fraud departments to focus on events beyond the front line.